Carbon Credits: what they really are (and why they matter)

Over the past two posts, I wrote about the electrification of industry, and how sectors like material handling quietly became early laboratories of that transition.

Electrification brings many advantages.

But it also produces something new.

Measurable emissions.

Once energy consumption becomes measurable, carbon emissions can be quantified.

And once emissions are quantified, they can enter a broader system of accounting.

This is where carbon credits come in.

In simple terms, a carbon credit represents one tonne of CO₂ that has been avoided, reduced, or removed through a certified project.

But issuing such credits is not simply a declaration.

Projects must follow a rigorous process typically involving:

• Definition of a certified methodology

• Independent validation of the project

• Monitoring of emission reductions over time

• Third-party verification

• Registration of credits in a formal registry

Several international standards oversee these processes, including:

- Verra – Verified Carbon Standard (VCS)

- Gold Standard

- Climate Action Reserve

Only after this chain of validation can carbon credits be issued and traded.

The system is not perfect, and debates about its effectiveness are legitimate.

But one thing is clear.

As industries electrify and emissions become easier to measure, carbon accounting is becoming a new layer of industrial management.

Not only for compliance.

But increasingly as a strategic parameter in how companies design operations, supply chains, and investments.

Which raises a final question for this series.

If emissions can be measured and valued, how might this reshape future industrial business models?

That will be the focus of the next post.

News

-

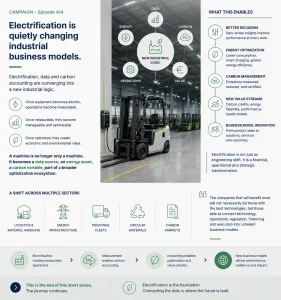

Electrification is quietly changing industrial business models

Over the past few posts, I wrote about electrification, material handling, and carbon accounting. At first glance, these topics may seem separate. They are not. They are gradually converging into…

-

Material Handling: an early laboratory of electrification

Last week, I started a short series of posts about the electrification of industry. The discussion is often framed at a national level — energy sovereignty, infrastructure, or public policy. But…

-

Electrification is already here. We just rarely notice it.

In recent weeks, the French press has echoed the government’s renewed push toward electrification. As Sébastien Lecornu recently stated when presenting elements of the national strategy: “L’électrification du pays est…

-

Rare Earth Recycling: Europe’s Fast Track to Supply Chain Resilience

A few weeks ago, I wrote about the pause that follows the end of a long chapter, and how that silence helps clarify where one can be genuinely useful next.…

-

The Day After: What a Pause Reveals About Leadership and Change

Last month, I handed in my badge and my car keys.The surprising part is not the end itself.It’s what becomes visible the day after.When the calendar empties, a few things…